Dec

2022

A new uranium bull market is underway, driven by the race to net zero

DIY Investor

20 December 2022

![]()

Energy underpins our civilization and is vital for the survival of society; it is needed heat and light up homes, power factories and transport food, people and everything else – writes Tom Bailey, Head of ETF Research at HANetf

Energy underpins our civilization and is vital for the survival of society; it is needed heat and light up homes, power factories and transport food, people and everything else – writes Tom Bailey, Head of ETF Research at HANetf

Since the 19th century, we have relied upon oil, gas and coal for this. These proved to be cheap, reliable and abundant energy sources, providing the backbone of the world’s immense economic progress over the past 150 years.

However, this has come at a cost. It is now widely accepted that the CO2 released when fossil fuels are burned is heating up the planet to catastrophic effect, with far-reaching humanitarian consequences.

In response, governments around the world have set ambitious net-zero targets. In total, 83 countries, responsible for 74.2% of global greenhouse gas emissions, have communicated a net-zero target.

A core part of these goals will be decarbonizing electricity generation. Over 40% of energy-related CO2 emissions are due to the burning of fossil fuels for electricity generation.

Therefore, to make significant progress in achieving their net-zero goals, countries need to invest in infrastructure that can replace carbon-producing energy sources with carbon-free energy sources. Changes on the margin will not suffice. Small increases in renewable energy sources and incremental moves toward electric vehicles are considered low-impact tweaks that will barely move the needle.

By contrast, nuclear power has the potential to provide high-impact change that can significantly move the needle. Given that nuclear power can provide an appealing solution, sentiment has turned much more positive in recent years. Environmental advocates face the tough choices required to

decarbonize economies. While there are still holdouts, the political tone toward nuclear power is on the upswing.

Three reasons nuclear power is an appealing investment

1) Nuclear is reliable

For a national, state or local utility, the appeal of nuclear power starts with its reliability. Regions with nuclear power plants deploy reactors round-the-clock, using nuclear as the baseload power source for electric grids. All other power sources depend on less-reliable inputs — whether that’s fuels with volatile prices or natural conditions that are unpredictable and intermittent, like wind, solar and hydroelectric.

2) Nuclear is efficient

One uranium fuel pellet — about the size of a gummy bear — is the energy equivalent of three barrels of oil, or one ton of coal, or 17,000 cubic feet of natural gas, according to the American Nuclear association. The energy density of uranium translates to huge efficiencies. Efforts to reprocess or recycle spent fuel in nuclear plants extend uranium’s efficiency further. Enriched uranium only uses about 4% of the potential energy in the first cycle through a reactor. As the technology advances to make it more economically viable to recycle fuel, the efficiency of nuclear is likely to rise even higher.

3) Nuclear is clean

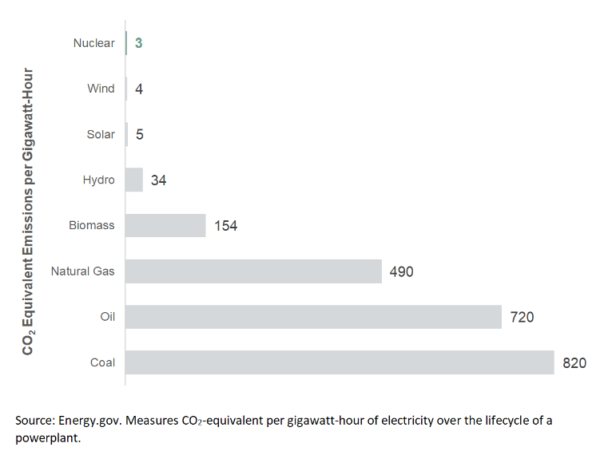

Nuclear energy generates the lowest greenhouse gases of any power source, period. Over the full lifecycle of nuclear power production, each gigawatt-hour of electricity contributes about three CO2 equivalent emissions per gigawatt-hour of electricity, which is in line with wind and solar. Hydroelectric power sources generate 10 times more CO2 equivalent emissions; oil and coal generate 240 and 273 times more, respectively.

A new uranium bull market?

The changing sentiment toward nuclear power is driving the first signs of a new uranium bull market.

Since the advent of nuclear energy, uranium, as a commodity, has seen two other bull markets. The first was in the 1970s. The defining feature of that decade was an energy crisis, due to the OPEC oil embargo, and geopolitical tensions, in the form of the Cold War. The energy crisis encouraged governments to turn to nuclear energy while the Cold War saw governments stockpile uranium for potential military use. This strong demand resulted in a bull market between 1973 to 1978.

The next bull market came during the commodity supercycle of the 2000s. Surging oil prices resulted in many expecting a renaissance in nuclear energy. That bull market ended with the onset of the Global Financial Crisis and the requestioning of nuclear energy following the 2011 tsunami-driven accident at Fukushima, Japan.

The reaction to that incident, however, is increasingly seen as rash and misguided. Today, we believe we are at the start of a new bull market in uranium. Crucially, there is a deficit in uranium supply. The production of uranium has simply not kept pace with the pace of new reactor requirements.

Until recently, the gap between production and demand had little impact on the spot price. This was due to the availability of stockpiles made available at the end of the Cold War. With the de-

escalation of tensions, weapons stockpiles were released for use in power plants. However, the availability of that supply is coming to an end. Uranium miners will need to step up production to plug the gap.

More information about Sprott Uranium Miners UCITS ETF here >

Sprott Uranium Miners UCITS ETF launches in London to tap into nuclear energy trend

Important Information

Communications issued in the UK (ETFs and ETCs)

The content in this document is issued by HANetf Limited (“HANetf”) and approved by Privium Fund Management (UK) Limited (“Privium”). HANetf are an appointed representative of Privium, which is authorised and regulated by the Financial Conduct Authority.). HANetf is registered in England and Wales with registration number 10697042.

Communications issued in the European Economic Area (“EEA”) relating to ETFs

The content in this document is issued by HANetf Management Limited (“HML”) acting in its capacity as management company of HANetf ICAV. HML is authorised and regulated by the Central Bank of Ireland. HML is registered in Ireland with registration number 621172.

Communications issued in the EEA relating to ETCs

The content in this document is issued by the relevant Issuer.

The Issuers

1. HANetf ICAV, an open-ended Irish collective asset management vehicle issuing under the terms in the Prospectus and relevant Supplement for the ETF approved by the Central Bank of Ireland (“CBI”) (“ETF Prospectus”) is the issuer of the ETFs. Investors should read the current version of the ETF Prospectus before investing and should refer to the section of the ETF Prospectus entitled ‘Risk Factors’ for further details of risks associated with an investment in the ETFs. Any decision to invest should be based on the information contained in the ETF Prospectus.

2. HANetf ETC Securities plc, a public limited company incorporated in Ireland, issuing:

i. the precious metals ETCs under the terms in the base prospectus approved by both the Central Bank of Ireland (“CBI”), the UK Financial Conduct Authority (“FCA”) and the final terms of the precious metals (together, “Metals ETC Prospectuses”);

ii. the carbon securities ETCs under the terms in the base prospectus approved by the UK Financial Conduct Authority (“FCA”) and the relevant final terms of the carbon securities (together, “FCA Carbon ETC Prospectus”); and

iii. the carbon securities ETCs under the terms in the base prospectus approved by the Central Bank of Ireland (“CBI”) and the final terms of the carbon securities (together, “CBI Carbon ETC Prospectus”).

Investors should read the latest versions of the relevant ETC prospectus before investing and should refer to the section of the relevant ETC prospectus entitled ‘Risk Factors’ for further details of risks associated with an investment in the ETCs. Any decision to invest should be based on the information contained in the relevant ETC prospectus.

3. ETC Issuance GmbH, a limited liability company incorporated under the laws of the Federal Republic of Germany, issuing under the terms in the Base Prospectus approved by the Bundesanstalt für Finanzdienstleistungsaufsicht (“BaFin”) and the final terms (“Cryptocurrency Prospectus”) is the issuer of the ETC Group ETCs. Investors should read the latest version of the Cryptocurrency Prospectus before investing and should refer to the section of the Cryptocurrency Prospectus entitled ‘Risk Factors’ for further details of risks associated with an investment in the ETCs contained in the Cryptocurrency Prospectus. Any decision to invest should be based on the information contained in the Cryptocurrency Prospectus.

The ETF Prospectus, Metals ETC Prospectus, FCA Carbon ETC Prospectus, CBI Carbon ETC Prospectus and Cryptocurrency Prospectus can all be downloaded from www.hanetf.com.

This communication has been prepared for professional investors, but the ETCs and ETFs set out in this communication (“Products”) may be available in some jurisdictions to any investors. Please check with your broker or intermediary that the relevant Product is available in your jurisdiction and suitable for your investment profile.

Past performance is not a reliable indicator of future performance. The price of the Products may vary and they do not offer a fixed income.

This document may contain forward looking statements including statements regarding our belief or current expectations with regards to the performance of certain assets classes. Forward looking statements are subject to certain risks, uncertainties and assumptions. There can be no assurance that such statements will be accurate and actual results could differ materially from those anticipated in such statements. Therefore, readers are cautioned not to place undue reliance on these forward-looking statements.

The content of this document is for information purposes, and does not constitute an investment advice, recommendation, investment research or an offer for sale nor a solicitation of an offer to buy any Product or make any investment.

An investment in an exchange traded product is dependent on the performance of the underlying asset class, less costs, but it is not expected to track that performance exactly. The Products involve numerous risks including among others, general market risks relating to underlying adverse price movements in an Index (for ETFs) or underlying asset class and currency, liquidity, operational, legal

and regulatory risks. In addition, in relation to Cryptocurrency ETCs, these are highly volatile digital assets and performance is unpredictable.

The information contained on this document is not, and under no circumstances is to be construed as, an advertisement or any other step in furtherance of a public offering of securities in the United States or any province or territory thereof, where none of the Issuers (as defined below) or their Products are authorised or registered for distribution and where no prospectus of any of the Issuers has been filed with any securities commission or regulatory authority. No document or information on this document should be taken, transmitted or distributed (directly or indirectly) into the United States. None of the Issuers, nor any securities issued by it, have been or will be registered under the United States Securities Act of 1933 or the Investment Company Act of 1940 or qualified under any applicable state securities statutes.

Alternative investments Commentary » Alternative investments Latest » Commentary » Exchange traded products Commentary » Exchange traded products Latest » Latest » Mutual funds Commentary

Leave a Reply

You must be logged in to post a comment.