Aug

2025

The best Stocks and Shares ISA providers for 2025

DIY Investor

27 August 2025

We take a look at the best UK Stocks and Shares ISA providers for 2025, focusing on fees, choice of investments and client ratings…by Jo Groves

Choosing the best Individual Savings Account (ISA) provider can make all the difference when it comes to growing your investments tax-free.

Whether you’re looking for low fees, a wide range of investment options or top-tier customer support, we’ve compiled a list of the best ISA providers in the UK to help you navigate through the multitude of options on offer.

In our frequently asked questions below, we provide an overview of how stocks & shares ISAs work, including how much you can invest, the types of investments you can hold and the fees you’ll pay.

Why fees matter…

It’s important to choose a provider whose fee structure matches your investing style: frequent traders will look for a platform with low trading fees while buy-and-hold investors will be more focused on platform fees (which we’ll explain below).

It’s easy to forget that even a small difference in fees can add up to thousands of pounds over time, as shown in the chart below.

By way of example, an initial investment of £50,000 with an annual growth rate of 9% could grow into a pot of £117,000 after 10 years and £273,000 after 20 years with a flat platform fee.

Looking at percentage-based platform fees, the portfolio would be worth £14,000 and £38,000 less over 20 years for a 0.50% and 1.0% platform fee compared to 0.25%. And if you achieve a higher annual return on your investments, this gap could widen further…

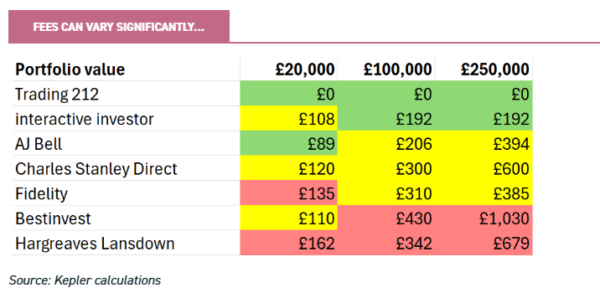

Fees are set out in detail below but the following table summarises our indicative fee calculation by provider, with green being the cheapest and red the most expensive.

The best ISA providers

Below we set out our pick of the best ISA providers, with the methodology behind our rankings set out below (including the basis of our fee calculations).

key data

| Platform fee on funds (up to £250,000) | Indicative portfolio fees | |

| £3.99 | Investor Essentials (up to £50,000): £4.99 per month Investor (above £50,000): £11.99 per month |

£20,000: £108 £100,000: £192 £250,000: £192 |

Why we picked it

interactive investor (ii) has over 430,000 clients and is owned by fund manager abrdn but still offers third party funds. It also offers a trading account, SIPP and Junior ISA but does not offer a Lifetime ISA.

Clients have a wide range of investment options, with more than 40,000 investment options, including over 3,000 funds, 1,000 ETFs and a selection of investment trusts. It also offers managed funds and ‘quick-start’ multi-asset funds.

interactive investor is one of the few platforms with a flat (rather than percentage-based) platform fee, making it a particularly cost-effective option for investors with higher-value portfolios.

The Investor Essentials plan (for portfolios up to £50,000) costs £4.99 per month which includes a trading account and ISA but costs a further £5 per month to add a SIPP.

The Investor plan (for £50,000-plus portfolios) costs £11.99 per month and includes a trading account, ISA and Junior ISA, with an additional £10 per month to add a SIPP.

Moving onto trading fees, ii charges £3.99 for funds and UK and US shares, rising to £9.99 for other international shares. The Investor plan includes a free monthly trade and the Super Investor plan (£19.99 per month) includes four free monthly trades.

In terms of extras, ii pays interest on uninvested cash held in an ISA and provides customer support by phone and live chat. It also provides extensive research on its website and has a rating of 4.7 on Trustpilot.

Clients are automatically opted into the voting and information service (unless they opt out) and are notified by email when meetings are announced. Clients can place their votes on the app-based ‘voting mailbox’ service.

Overall, interactive investor is an excellent all-rounder, offering a flat platform fee for investors with higher value portfolios, alongside a broad universe of investment options and a competitive trading fee.

Key data

| Trading fee on shares | Platform fee on funds (up to £250,000) | Indicative portfolio fees |

| £5.00 | 0.25% | £20,000: £89 £100,000: £206 £250,000: £394 |

Why we picked it

AJ Bell is a FTSE 250 company with over 540,000 clients and offers a dealing account, SIPP, Junior ISA and Lifetime ISA.

Clients have a wide range of investment options, with over 15,000 UK and international shares, 3,000 ETFs, 4,000 funds and 380 investment trusts. It also offers a range of ready-made managed and non-managed portfolios.

In terms of fees, AJ Bell has one of the lowest platform fees amongst the mainstream providers both by percentage and tier value. The platform fee is 0.25% on the first £250,000, 0.10% on the next £250,000 and no fee over £500,000. There is a separate platform fee of 0.25% for share-based investments (including investment trusts and ETFs) which is capped at £3.50 per month (£42 per year).

Moving onto trading fees, it charges one of the lower fees of £5.00 for UK and international shares but charges £1.50 for trading in funds. Regular traders benefit from a reduced fee of £3.50 on shares if they trade 10 or more times in the previous month.

In terms of extras, AJ Bell pays interest on uninvested cash held in an ISA, has an easy-to-use app and provides customer support by phone and live chat. It should also be commended on the quality of its research, together with its regular webinars and podcasts. It has a rating of 4.9 on Trustpilot, the highest among our selected group.

Recent developments have cast a spotlight on voting by retail investors and AJ Bell has launched a new service for electronic voting via third-party provider Broadridge. Clients are notified of corporate actions and upcoming meetings and can also access a calendar of upcoming meetings via their account on the website.

Overall, AJ Bell is a good all-rounder, offering competitive fees and the second-highest range of investment options.

Key data

| Trading fee on Uk shares | Platform fee on funds (up to £250,000) | Indicative portfolio fees |

| No charge | Standard: £4.99 per month | £1,000: £60 £10,000: £60 £20,000: £60 |

Why we picked it

Freetrade is a UK fintech with over one million users. It was acquired by IG in early 2025 but will remain a standalone brand. It offers an investment account, ISA and SIPP but does not currently provide a Junior or Lifetime ISA.

Clients can access almost 6,000 UK, European and US shares, as well as 600 ETFs and investment trusts. Actively-managed funds are only available through the Plus plan. Freetrade also offers fractional US shares.

In terms of fees, Freetrade charges £4.99 per month for its standard plan, which includes a trading account, and £9.99 per month for its plus plan, which also includes a SIPP. The plus plan also offers a lower foreign exchange fee, a higher interest rate on uninvested cash and priority customer service. It charges no trading fees on shares or funds.

However, it’s more of a no-frills option with limited research and support by online chat only, with one of the lower TrustPilot ratings of 4.2. While it perhaps lacks the depth of research and range of accounts offered by the mainstream providers, it’s a solid choice for cost-conscious investors.

key data

| Trading fee on UK shares | Platform fee on funds (up to £250,000) | Indicative portfolio fees |

| No charge | No charge | £20,000: £0 £100,000: £0 £250,000: £0 |

Why we picked it

Trading 212 is a UK fintech that offers commission-free trading and has 3 million global lifetime funded accounts. It’s a private company but is profit-making and FCA-authorised. It also offers an investment account but no SIPP, Junior ISA or Lifetime ISA.

Clients can choose from over 13,000 UK and international shares and ETFs but it does not offer actively-managed funds. It also has a range of ready-made ‘model pies’ comprised of ETFs.

Trading 212 charges no trading or platform fees and pays one of the highest interest rates on uninvested cash. However, it’s more of a no-frills option with limited research and support by online chat only. It has a Trustpilot rating of 4.6.

Trading 212 provides voting on a ‘best effort’ basis and emails clients ahead of company meetings, together with a website link to cast their vote.

Overall, Trading 212 is likely to appeal to frequent traders or investors looking for a basic, low-cost provider although it’s worth noting that it has one of the highest Trustpilot ratings amongst our selected providers.

key data

| Trading fee on UK shares | Platform fee on funds (up to £250,000) | Indicative portfolio fees |

| £11.95 | 0.45% | £20,000: £162 £100,000: £342 £250,000: £679 |

Why we picked it

HL is one of the largest DIY investment platforms in the UK with over 1.9 million clients and a recent shift to private ownership. HL offers a full suite of products, including a fund and share account, SIPP, Junior ISA and Lifetime ISA.

Clients have a wide range of more than 14,000 investment options, including UK and international shares and over 4,000 funds, 1,900 ETFs and 300 investment trusts. It also offers managed funds and multi-asset funds.

HL is one of the more expensive mainstream providers, both by percentage and tier value, with a platform fee of 0.45% on the first £250,000 of funds, 0.25% for the portion between £250,000 and £1 million, 0.1% on the portion between £1 to £2 million and no charge over £2 million. There is a maximum cap of £3.75 per month (£45 per year) for share-based investments.

It also charges the highest trading fee of £11.95 although there is no trading fee for funds. There is a reduced trading fee for frequent traders, being £5.95 and £8.95 (based on 10-19 and 20-plus trades respectively in the previous month).

In terms of extras, HL pays interest on uninvested cash and provides customer support by phone and online messaging. It also provides extensive research on its website, including podcasts and webinars. However, it has a mid-range rating of 4.4 on Trustpilot and is often commended for the quality of its phone support.

HL notifies clients of upcoming votes by secure message and has launched a new service offering electronic voting via its website.

Overall, HL may appeal to investors willing to pay for a premium service, with an excellent choice of investments, research offering and customer service. The platform fee for share-based investments is a lower-cost option due to the cap, however trading fees could add up for frequent share traders.

key data

| Trading fee on UK shares | Platform fee on funds (up to £250,000) | Indicative portfolio fees |

| £7.50 | 0.35% | £20,000: £135 £100,000: £310 £250,000: £385 |

Why we picked it

US fund giant Fidelity has over 1.6 million customers in the UK but, unlike some of its fund management peers, offers a wide range of third-party funds in addition to Fidelity funds. It also offers an investment account, SIPP and Junior ISA but no Lifetime ISA.

Clients can choose from over 2,400 UK and international shares, 2,900 funds, 400 ETFs and 170 investment trusts, although this is at the smaller end amongst our group. Fidelity has a range of ready-made and managed portfolios, as well as offering personalised finance advice.

Fidelity is unusual in charging a non-tiered platform fee, meaning that you pay one fee based on the total value of your portfolio (across all accounts), rather than different fees on different portions. This may appeal to investors with higher-value portfolios that can benefit from the lower platform fee that kicks in at £250,000.

The platform fee is 0.35% up to £250,000 (capped at £90 per year for sub-£25,000 portfolios with no regular savings plan in place), 0.20% from £250,000 to £1 million and, for £1 million plus portfolios, 0.20% on the first million and no charge beyond that. There is a maximum fee of £7.50 per month (£90 per year) for share-based investments.

It charges one of the higher trading fees of £7.50 although there is no trading fee for funds.

In terms of extras, Fidelity pays interest on uninvested cash held in an ISA and provides customer support by phone and online messaging. It also provides a good level of research on its website, including podcasts, and has a mid-range rating of 4.4 on Trustpilot.

Clients have to opt in and sign up to third-party provider Broadridge to receive notifications about upcoming meetings. Once signed up, clients can vote online via the Broadridge portal.

Overall, Fidelity may be a good option for investors with higher-value portfolios, which can benefit from reduced platform fees, although the share trading fee and more limited set of investments may deter frequent traders.

key data

| Trading fee on UK shares | Platform fee on funds (up to £250,000) | Indicative portfolio fees |

| £4.95 | 0.4% | £20,000: £110 £100,000: £430 £250,000: £1,030 |

Why we picked it

Bestinvest is owned by wealth manager Evelyn Partners and has over 50,000 clients. It also offers an investment account, SIPP and Junior ISA but not a Lifetime ISA.

Clients can choose from over 1,100 shares, 1,600 funds, 330 ETFs and 280 investment trusts. It offers one of the widest ranges of ready-made portfolios, categorised by expert (maximising return), smart (low-cost, passive funds), direct (shares and bonds) and sustainable (ESG).

For funds and UK shares, the platform fee is 0.4% up to £250,000, 0.2% from £250,000 to £500,000, 0.1% from £500,000 to £1 million and no charge above £1 million. There is a lower fee for US shares and ready-made portfolios, being 0.2% up to £250,000 (and the same as above thereafter). However, it’s worth noting that the foreign exchange fee of 0.95% on non-UK shares is towards the upper end of our group.

It charges a mid-range trading fee of £4.95 on UK shares and no fee on funds and US shares. Bestinvest provides a telephone and live facility, as well as free one-on-one coaching. It provides a good level of research, including the annual “Spot The Dog” review of underperforming funds but has one of the lower Trustpilot ratings amongst our selected providers at 4.3.

Bestinvest doesn’t typically notify clients of upcoming votes but clients can provide their voting instructions by email or secure message.

Overall, Bestinvest is a decent all-rounder but offers a more limited range of investments and the platform fee becomes expensive on higher-value portfolios (without a cap on share-based investments). However, it provides a good range of ready-made portfolios and customer support.

key data

| Trading fee on UK shares | Platform fee on funds (up to £250,000) | Indicative portfolio fees |

| £10 | 0.3% (subject to £60 minimum & £600 maximum) | £20,000: £60 £100,000: £300 £250,000: £600 |

Why we picked it

Charles Stanley is a privately-owned company, having been bought by US investment firm Raymond James in 2022. It offers wealth management services in addition to DIY investing via Charles Stanley Direct. Clients have the choice of an investment account, ISA, Junior ISA and SIPP but no Lifetime ISA.

It offers a decent range of 12,500 investments, including shares, funds, ETFs and investment trusts, in addition to a selection of managed portfolios.

Charles Stanley Direct charges a platform fee of 0.30% on the value of investments held across all accounts, subject to an annual minimum fee of £60 and maximum fee of £600. There is no platform fee on the managed portfolios.

It charges one of the higher trading fees of £10 on shares and £4 on funds, however customers receive £50 worth of trading credits every 6 months.

Charles Stanley Direct provides a comprehensive level of research, including market commentary and webinars but has the lowest Trustpilot ratings of our selected providers at 3.8.

It doesn’t typically notify clients of upcoming votes but clients can provide their voting instructions by email or secure message.

Overall, Charles Stanley may appeal to investors with higher-value portfolios due to the annual platform cap, or frequent traders looking to make use of the trading fee credits.

Methodology

To come up with our list of best stocks and shares ISA providers, we applied three main criteria. Our focus was on whether providers:

- charged competitive trading and platform fees

- offered customers a wide range of third-party investments

- had a good rating on consumer review site Trustpilot

We also considered other features such as our personal experience of the providers, whether ready-made portfolios were available and the option to hold other accounts such as Self-Invested Personal Pensions (SIPPs).

We calculated indicative fees on the following basis:

- Platform fees: for flat platform fees, we picked the cheapest option for an ISA.

- Trading fees: 12 trades per year, split equally between funds and UK shares. If a provider offered free monthly trades, we assumed that half of these could be used and for Charles Stanley Direct, we offset trading fees against the £100 of annual trading credits.

- Portfolio values: £20,000, £100,000 and £250,000.

- Split of portfolio: 50% UK shares/ETFs and 50% funds.

Frequently asked questions

What is a stocks & shares ISA?

A stocks & shares ISA (S&S ISA) is a tax-efficient investment account that allows you to invest in a wide range of assets such as shares, bonds and funds. Unlike a cash ISA, which simply earns interest, a S&S ISA gives you the potential for higher returns by tapping into the stock market.

According to research by Moneyfarm, the average cash ISA has returned 1.2% per annum over the last decade (to November 2024), compared to 9.0% for a traditional bond and equity ISA or 12.5% for a global equity portfolio. S&S ISAs are good for longer-term goals, such as saving for retirement or a future home, but there is a risk that investments can also go down in value.

However, the real appeal of a S&S ISA lies in its tax advantages: any capital gains, dividends or interest earned within the ISA are free from income tax and capital gains tax. You can invest up to £20,000 per year (based on the 2023/24 tax year) across all the types of ISAs you hold.

Who can open a S&S ISA?

To open a S&S ISA, you must be at least 18 years old and a UK resident for tax purposes and it’s a simple process that typically takes around 10-15 minutes to open online.

You can only open one S&S ISA per tax year but you don’t need to close old ones before opening a new one. You’re also free to transfer funds from existing ISAs if you want to consolidate or switch providers.

If you contribute to another type of ISA (such as a Cash or Lifetime ISA) during the same tax year, your combined contributions across all ISAs must not exceed the £20,000 annual allowance.

If you’re under 18, you can invest up to £9,000 per year in a Junior ISA, which can be transferred into an adult ISA (or withdrawn) when you become 18.

What can you invest in?

A S&S ISA offers a wide range of investment options to suit different goals and risk appetites. You can invest in individual company shares or opt for funds which pool your money with other investors to invest in a portfolio of assets. The range of investments will be determined by your ISA provider, with some offering thousands of different investment options.

There are two main types of funds to invest in:

- Actively-managed funds: these are professionally managed by fund managers who pick a

basket of investments such as equities, bonds or commodities. As a result, they typically charge a higher annual management fee of 0.5% to 1.0%. - Passively-managed funds: also known as index, tracker or exchange-traded funds (ETFs), these track an index such as the FTSE 100 or S&P 500 although there are more specialist options tracking commodities and property indices. They typically charge a lower annual management fee of 0.1% to 0.5%.

Alternatively, less-experienced investors may wish to consider the following managed options:

- Ready-made portfolios: these are offered by most of the mainstream platforms and provide a diversified portfolio of funds, usually categorised by risk appetite.

- Robo-advisers: these aim to provide a halfway house between personalised financial advice and DIY investing. Investors complete a questionnaire to determine their goals and appetite for risk which is used to build an automated portfolio.

- Financial advisers: these provide individual, tailored advice on portfolio construction and, as a result, are likely to be the most expensive option.

What fees will you pay?

It’s important to understand the fees involved as these can significantly impact your returns over time. There are three main types of fees:

- Platform fee: this is a fee for holding investments on the provider’s platform, usually calculated as a percentage of your total portfolio value (typically 0.25%-0.45% per year). Platform fees may be capped at a maximum amount per year and can vary according to whether you hold share-based investments (company shares, exchange-traded funds (ETFs) and investment trusts) or funds. Alternatively, a small number of providers offer a flat fee.

- Platform fees are usually tiered, meaning that you’ll pay a lower platform fee on the portion of your portfolio over certain thresholds, for example, 0.25% up to £250,000, then 0.1% on the portion between £250,000 to £500,000 and no fee on the portion above £500,000.

- Trading fee: you’ll typically pay a trading fee of £4 to £12 for buying shares (including ETFs and investment trusts) although some platforms offer commission-free trading. Trading fees for funds are generally lower, or often zero, and frequent traders often pay a lower fee, usually based on the number of trades in the previous month or quarter.

- Fund management fees: as mentioned above, you’ll pay an annual management fee for investing in funds, which is typically between 0.1% and 1%.

In addition, if you trade non-UK shares, you will typically pay a foreign exchange fee of 0.5% to 1.0% and you may be charged a higher trading fee for these shares. You will also be charged Stamp Duty Reserve Tax (SDRT) of 0.5% on trades in individual UK company shares.

Leave a Reply

You must be logged in to post a comment.