Oct

2025

Pickafund: 5 Things to consider when buying a VCT

DIY Investor

10 October 2025

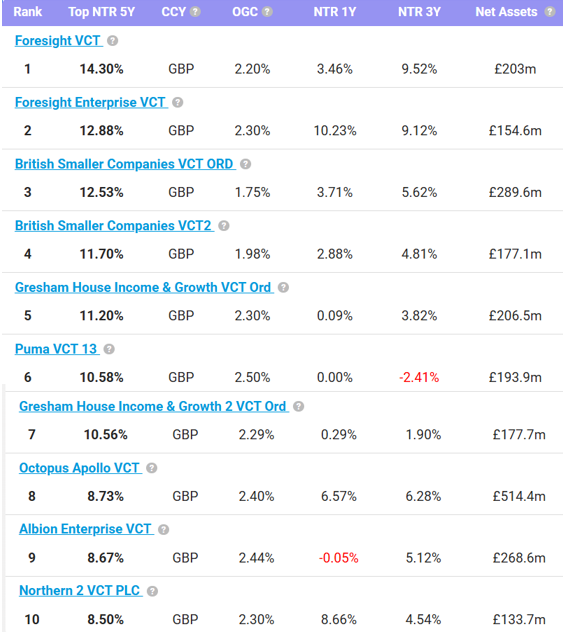

Top performing VCTs by 5 Year Net Total Return

(Returns are shown annualised)

Data correct as at 29-Sep-2025. Past performance is no guarantee of future returns.

To view an updated version of the above ranking table, click here then select your preferred criteria (Net Total Return 1Y, 3Y, 5Y or 10Y) from the “Compare by” drop-down then scroll down to the “Top fuds in this category” section at the bottom of the page.

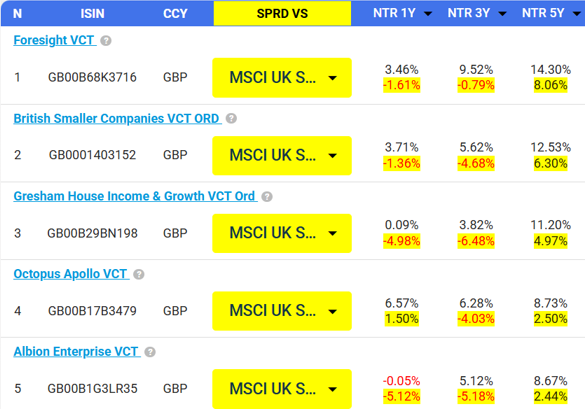

Top VCTs past performance against MSCI UK Small cap ETF

(Spreads vs benchmark are highlighted in yellow. Returns are shown annualised)

Data correct as at 29-Sep-2025 Past performance is no guarantee of future returns.

Table of contents:

Introduction

1. Focus on Net Total Returns, Not Just Share Price Performance

2. Understand the Discount to NAV – It Affects Your Starting Point

3. Check How Long the VCT Has Been Running

4. Be Aware of Performance Fees

5. Management Continuity Matters

Introduction

Key features of VCTs:

- VCTs are UK specific closed-ended funds which invest in high-risk, small or early-stage UK companies (unquoted as well as AIM listed) that qualify under HMRC rules, to provide them with development & expansion funding.

- In order to attract capital to this vital but risky part of the economy (small and early-stage companies have a higher risk of failure), the UK government uses tax incentives as mitigation for the risk investors take on.

Tax reliefs provided for VCT investments comprise:

- 30% income tax relief on VCT investments up to £200,000 per tax year. This relief is only available if:

- You buy new shares directly from the VCT (usually via a VCT offer).

- You hold the shares for at least 5 years.

- Tax-free dividends from VCT shares.

- No Capital Gains Tax (CGT) on disposal of VCT shares.

- 30% income tax relief on VCT investments up to £200,000 per tax year. This relief is only available if:

- They’re listed on the London Stock Exchange, meaning you can buy and sell VCT shares like other publicly traded stocks. Buying VCT shares via the stock exchange (i.e., from another investor) does not qualify for income tax relief.

Population:

By type:

- AIM VCTs (primarily invest in quoted AIM companies)

- Other (typically generalist VCTs who tend to invest a majority of their portfolio in private unquoted companies)

Key differences between AIM and generalist VCTs are:

| AIM VCTs | Generalist VCTs | |

| Valuation | More transparent – daily exchange price available for underlying investments | Less transparent – theoretical valuation updated periodically for underlying investments |

| Volatility | More volatile – Exposed to broad public markets downturns | Less volatile – Less exposed to public markets fluctuations |

Main VCTs by family:

Below we list 5 points to pay particular attention to when investing in VCTs

1. Focus on Net Total Returns, Not Just Share Price Performance

When reviewing how a VCT has performed in the past, don’t just look at the change in its share price.

Most investment platforms will show “price returns,” which exclude dividends and other distributions. But with VCTs, distributions (often paid out as tax-free dividends) are a major part of the overall return.

To get a true picture of performance, look at the net total return, which includes both the share price movement and the value of all distributions paid.

Strong:

- over the past 5 to 10 years, annualised total return net of fees in the 7–10% range or above especially with consistent dividend payouts (a dividend yield of 5 to 8%, tax-free, is typical among income-focused VCTs).

>>Net total returns can be viewed on Pickafund, as illustrated below.

You can also sort and filter a list of VCTs (e.g. all VCTs) using net total returns criteria (like “Net total return 5Y” or “Net total return 10Y”).

When filtering, you have the option to view only funds from a certain quartile. For instance, selecting 1st quartile for Net Total Return 5 Year will give you the top 25% of the population ranked by Net Total Return 5 Year.

2. Understand the Discount to NAV – It Affects Your Starting Point

When buying VCT shares from the VCT provider directly, they are typically issued at Net Asset Value (NAV) — that’s the value of the underlying investments. But on the secondary market (when you buy or sell existing shares), they may trade at a discount (i.e. below NAV). If you buy newly issued shares and then they trade at a significant discount, your investment could be down on paper right away.

While VCTs are designed to be held for at least five years (to retain the 30% income tax relief), that discount will still matter when you eventually sell. A wide discount at the exit point could reduce your final return and offset some of the benefit you got from the tax break.

Also, check if the VCT has a discount control mechanism — this is a policy to buy back shares to keep the share price close to the Net Asset Value (NAV), which can help reduce volatility and support investor confidence.

Good: Trade at a discount of 0–5% to NAV (or at a premium but that’s rare these days).

Poor: Trade at 15%+ discount to NAV, especially in the absence of a clear buyback policy or if there is poor past performance.

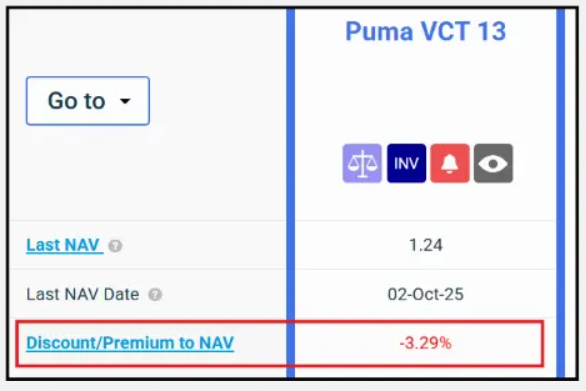

>>With Pickafund you can see the premium/discount to NAV for a VCT on its Detailed View page (just click on the VCT name to access it then go to section Price):

Click to see Puma VCT 13 Detailed View page

You can also sort a list of VCTs (e.g. all VCTs) using the criteria “Premium/discount to NAV” (logged in users only).

3. Check How Long the VCT Has Been Running

The age of the VCT matters. If the VCT has been recently launched, a large portion of its capital may still be held in cash while the managers look for suitable investments. That means:

- You won’t get a clear picture of the investment strategy’s success from historical performance alone.

- Early-stage portfolios are riskier because they’re unproven.

- Newer VCTs often have smaller asset bases, which limits economies of scale and can lead to higher relative costs.

In short, the more established the VCT, the more useful its track record is in assessing how well the manager selects and supports early-stage businesses. It doesn’t mean new VCTs won’t end up doing well in the future, they are just riskier.

Good:

- Established 7+ years ago with a mature, fully invested portfolio which would have seen some exits already. 7 to 10 years corresponds approximately to a typical private equity fund life cycle with investment phase, holding/value creation phase and then exit phase.

- Net assets > £100 million – larger size can lead to better deal access, cost efficiency, and diversification.

Weaker:

- Launched <2 years ago, with over 30–40% in cash and less investment track record to judge (in particular, no exit would have taken place).

- Net assets < £50 million – likely higher ongoing costs as % of assets.

>>With Pickafund, you can view the creation date of a VCT and how many years it has been in existence on the Detailed View page (just click on the VCT name to access it then go to section General):

➤Click to see British Smaller Companies VCT Detailed View page

You can also sort and filter a list of VCTs (e.g. all VCTs) using the criteria “Years since launch” (logged in users only).

>>>With Pickafund, you can see the net assets number for a VCT on its Detailed View page (just click on the VCT name to access it then go to section Portfolio):

➤Click to see British Smaller Companies VCT Detailed View page

You can also sort and filter a list of VCTs (e.g. all VCTs) using the criteria “Net assets”

4. Be Aware of Performance Fees

Most VCTs charge a performance fee in addition to ongoing charges. A typical rate is around 15–20% of profits above a certain hurdle, such as a target return or benchmark. However, if you see a performance fee that’s significantly higher than this, it’s worth questioning whether the extra cost is justified. Over time, high fees can eat into your returns — especially in a structure like a VCT, where overall returns may already be modest compared to higher-risk venture capital funds.

Good: 15–20% performance fee, usually above a hurdle rate (e.g. 7–8% annual return) and with a NAV high-water mark. Well-structured fees align manager and investor interests.

Red flag: performance fee > 20% then you need to really understand the construct of that performance fee (is there a hurdle rate or high water mark, what is the fee charged on exactly etc).

>>>With Pickafund, you can check the performance fee for a particular VCT on its Detailed View page (just click on the VCT name to access it then go to section Fees):

➤Click to see Octopus Apollo VCT Detailed View page.

5. Management Continuity Matters

As always with active funds, make sure that the track record you are looking at belong to the management team currently in place.

In VCTs particularly, success often hinges on a small investment team’s skill in finding and growing private companies. If a key manager leaves, it can materially impact performance.

Look for teams with long tenure, strong deal flow, and alignment with shareholders (e.g., significant co-investment).

>>With Pickafund, you can check who the managers of a particular VCT are and for how long they’ve been in the job, by going to the Detailed View page (just click on the VCT name to access it then go to section General):

➤Click to see British Smaller Companies VCT Detailed View page

You can also sort and filter a list of VCTs (e.g. all VCTs) using the criteria “Manager tenure” (logged in users only).

WARNING: VCTs (Venture Capital Trusts) are high risk, illiquid investments. They should form a small part of a diversified portfolio and are only suitable for experienced risk tolerant investors with a long term horizon. Also, tax rules can change and depend on personal circumstances. If in doubt, as always, speak to a financial advisor.

Pickafund.com offers information on funds but does not offer advice or recommendations for any particular course of action or product. Past performance and yields quoted should not be used as a reliable indicator of future returns. Investments can go up as well as down and you may get back less than what you originally put in, positive returns are not guaranteed. We don’t offer advice, so it’s important you understand the risks, if you’re unsure please consult a suitably qualified independent financial adviser.

Leave a Reply

You must be logged in to post a comment.