Feb

2026

8 FinTech Software Development Services Powering Digital Change

DIY Investor

10 February 2026

Digital transformation in financial services begins with comprehensive software system transformations which enable changes to core processes that include money transfer and risk assessment and financial product development. The last ten years have seen fintech software development services evolve into the primary technical framework which supports this industry transformation.

The financial industry depends on custom software solutions to maintain their market position and meet regulatory requirements. The financial companies partner with a skilled fintech software development company firm to update their outdated systems and develop new digital products and maintain their platforms for future needs.

1. Core Banking and Financial Platform Modernization

Financial institutions continue to use outdated core systems which were developed during a previous time period. The platforms face difficulties because they cannot process data in real time and they lack proper API connectivity and their development of new features takes too long. Core banking modernization aims to replace existing monolithic systems with modular systems which operate on cloud-ready infrastructure.

Digital banks such as Monzo and Revolut built modern cores to support instant payments and continuous product updates. Traditional banks use the same methods to achieve better operational flexibility while decreasing their technical debt.

This service enables financial organizations to react immediately to both regulatory and market fluctuations.

2. Payment Processing and Digital Wallet Infrastructure

People can see the effects of fintech innovation most clearly through payment systems. Payment software controls all routine financial activities which include mobile wallet transactions and international money transfers.

Payment development services provide support for all payment activities which include processing transactions and settling payments and preventing fraud and building wallet systems.

Stripe and Adyen demonstrate how their scalable payment systems enable companies to expand internationally while they fulfill local regulations. Custom payment software gives institutions greater control over performance, fees, and transaction data.

3. Investment and Wealth Management Platforms

The current investment practices of today depend on software solutions which serve as their main operational base. The technological systems which retail and institutional investors use for their platforms perform three functions which include managing portfolios and executing trades and delivering analytical results.

Wealth management development needs three components which include trading systems and portfolio management solutions and reporting systems and investor monitoring interfaces. Robinhood and eToro and Vanguard Digital Advisor platforms need software systems which can handle market changes and follow regulatory requirements.

The functionality of investment platforms establishes two user trust factors which determine their system usage duration.

4. Digital Lending and Credit Assessment Systems

Lending practices now use fast and complete automated systems to process loan applications. Borrowers now expect lenders to provide immediate decisions together with clear loan conditions.

Lending software development permits financial institutions to handle their loan originations and underwriting operations while tracking repayment and ensuring compliance.

Klarna and Affirm use automated scoring systems to make credit decisions within seconds while controlling their risk management process. The software solution enables lenders to expand their service range while maintaining their risk management procedures.

5. Fraud Detection and Financial Risk Solutions

The software development process at fintech companies relies on their fraud prevention efforts. The transaction monitoring systems which financial institutions use to detect suspicious activities benefit both their customers and their institutions.

Today’s fraud detection systems use machine learning algorithms together with established rules to monitor user activity as it happens.

Visa and Mastercard developed their artificial intelligence risk systems because their dedicated investment efforts enabled them to manage high transaction volumes. Security software protects businesses by decreasing financial losses while increasing customer trust.

6. Compliance, RegTech, and Reporting Platforms

Financial markets show ongoing changes to their regulatory requirements. Institutions must adhere to AML, KYC, GDPR, and all regional regulatory requirements.

The development of compliance software systems enables automated identity verification together with transaction monitoring and regulatory reporting functions.

Organizations use RegTech solutions to improve their audit response times while maintaining compliance with new policies through reduced manual work. The field of automation produces two main benefits which include reduced operational risk and enhanced transparency.

7. Customer-Facing Digital Banking Applications

Digital channels increasingly define how users interact with financial services. Mobile banking apps and trading platforms plus financial dashboards need to achieve security protection through their design while maintaining user-friendly functions.

Digital banking development focuses on secure authentication and intuitive user experience design together with personalized system features. BBVA and ING banks invested heavily in digital products to achieve higher customer engagement while decreasing their dependence on physical branch locations.

The software which customers directly interact with and the software which employees use to perform their tasks establish a direct link between customer satisfaction and brand loyalty.

8. Financial Data Analytics and Intelligence Systems

Data serves as the fundamental element which modern finance operations depend on. The analytics platforms of institutions enable them to extract insights from their transaction data and market signals and customer behavior patterns.

Financial intelligence software supports forecasting and risk modeling and strategic decision-making processes. Asset managers and hedge funds often use custom analytics tools to develop their trading strategies and control their market exposure.

Organizations make better decisions through data-driven platforms which also support their sustainable growth objectives.

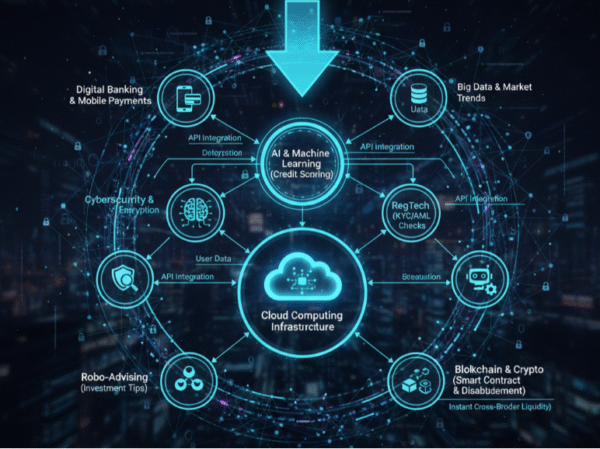

How these services work together in real fintech ecosystems

Financial institutions develop their operational systems through the combination of multiple services which function as integrated software ecosystems.

Digital banks depend on their modern core platform together with their custom payment processing system and their fraud detection tools and their compliance software and their customer-facing applications.

The process of connecting these elements demands both precise system development and extended strategic foresight. Organizations with integrated platforms can quickly adapt to both emerging regulations and changing market conditions.

Why software capability matters for investors

The software maturity of a system shows its capacity to maintain operational stability for an extended period according to an investor’s assessment. Fintech companies that develop their systems through proper architectural design will achieve better business performance when facing both regulatory changes and market competition.

Digital-first platforms experience decreasing expenses which improve their profitability as they expand their operations. The strong internal technology capabilities of fintech companies create operational efficiency which leads investors to prefer these firms for investment purposes.

Choosing the right fintech development strategy

Organizations typically choose between off-the-shelf products and custom development. Standard platforms enable organizations to launch their products quickly, while custom solutions provide organizations with the ability to create unique products which handle their specific business requirements.

The software selection process needs to support business objectives together with compliance needs and upcoming expansion plans in order to achieve successful digital transformation.

Conclusion

Fintech software development services sit at the core of digital change in finance. The services enable institutions to create new products while they handle risk management through their payment and lending and analytics and compliance functions.

Financial markets evolution creates a competitive advantage for organizations that develop flexible secure and scalable software solutions.

Leave a Reply

You must be logged in to post a comment.