Jan

2020

Reading the tea leaves ‒ what’s in store for China in 2020?

DIY Investor

5 January 2020

In this Q&A, China portfolio managers Charlie Awdry and May Ling Wee share their thoughts on the key challenges and opportunities that investors in China may face in the year ahead and how 2019 has influenced their outlook for the asset class.

Key takeaways:

- Trying to anticipate the nearer term outcome of the US-China trade talks is futile; the strategic rivalry between the two nations remains an ongoing issue

- The bedrock of the China investment case remains the consumer ‒ the team sees opportunities in internet services, healthcare and life insurance

- 2019 has shown that China’s leading companies are able to perform well despite a weaker, more challenging macro environment

What are the main risks that investors in Chinese equities should be cognisant of in 2020?

Geopolitical risks: quid pro quo retaliatory action

There is ultimately no easy resolution to the strategic rivalry between the US and China. Re-escalation of the trade and technology wars can happen at any time.

As investors, this is a difficult issue to navigate, especially when the US has many non-trade levers to pull. The trade war not only hurts China and the US, but also the global economy, as well as portfolio inflows into Chinese investments.

Hong Kong and the Communist Party’s reaction

The China Politburo Standing Committee’s stance towards the challenge to their authority appears to have hardened, suggesting that Hong Kong’s institutions and corporate sector could become more centrally controlled than before.

It could erode Hong Kong’s status as a separate jurisdiction under the ‘Basic Law’1 and its role as a global financial centre. The US Senate passing the Hong Kong Human Rights and Democracy Act will only add more complications to US-China relations.

Banking sector – small bank bailouts

Smaller regional banks in China continue to face liquidity challenges especially in the aftermath of three regional bank defaults this year; the implicit guarantee of previous bailouts has been removed.

While China’s large banks are relatively well capitalised, there is a possibility that they can be called upon to rescue failed smaller regional banks. We do not own Chinese banks in our portfolios.

What may be in store for 2020?

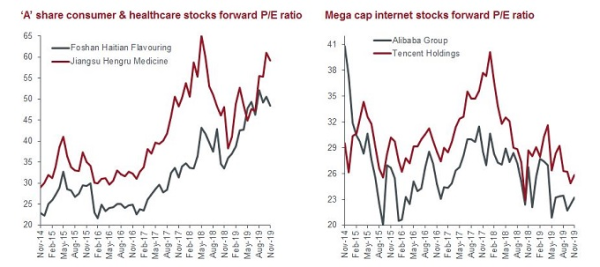

Growth at a reasonable price in mega cap internet stocks

Growth shares, especially in the Chinese healthcare and consumer sector have performed well year to date, as investors seek out stable sustainable growth.

Today, mega cap internet companies like Alibaba and Tencent, which continue to innovate to meet the needs of the Chinese consumer and businesses are trading at below average price-to-earnings multiples2 since the listing of the companies.

Source: Bloomberg, Janus Henderson Investors as at 26 November 2019. China ‘A’ shares are stocks that are denominated in yuan and listed on the Shenzhen and Shanghai stock markets. Past performance is not a guide to future performance.

Possible cyclical bottoming if easing steps up

While it is likely that China’s growth will slow into year end and early 2020, the expectation is for the government to step up both fiscal and monetary easing3 to stabilise growth.

Rate cuts (to lower borrowing costs) have been put in place, but have yet to translate into an increase in the volume of credit. If credit volumes return, infrastructure investments rise, and business confidence strengthens, we could see a possible near-term cyclical bottoming in the economy.

In our view, this is likely to be a more supportive backdrop for the better value, leading industrial and consumer cyclical companies (that tend to be more sensitive to changes in the economy) in China.

What are the key themes that you look to take advantage of when investing in China?

Consumption and services

Our view remains unchanged ‒ the Chinese consumer is the foundation of the investment case in China. Companies that can provide the right products and services to the consumer win ‘mind and wallet’ share.

The Chinese consumer is becoming more discerning; innovation by the large internet service companies allows them to meet the needs of the consumers that form China’s circa 850mn ‘netizens’.

Opening up of financial markets

China wants to encourage foreign investments into its equity and bond markets. Global allocations to the Chinese asset class are likely to increase given the inclusion of China ‘A’ shares in the MSCI Emerging Markets Index last year.

Through both the Shanghai/Shenzhen Stock and Bond Connect4, the Hong Kong Stock Exchange (HKEx) continues to provide a convenient means to access local asset markets.

HKEx could also benefit if more Chinese companies choose to dual list (in both mainland China and Hong Kong); favouring HKEx as an alternative listing to American depositary receipts (ADRs)5 where compliance with US regulatory and securities requirements is mandatory.

HKEx would then be the default overseas market, where the global pool of capital is sufficiently deep for Chinese companies to raise funds. A case in point is Alibaba’s decision to pursue its secondary listing in Hong Kong.

Ageing population: life insurance and healthcare

China’s ageing population’s collective wealth creates opportunities in service sectors such as life insurance and wealth management. Insurance penetration is low in China.

For the maturing workforce and China’s many increasingly wealthy entrepreneurs, the desire for wealth protection and asset growth is becoming stronger as these groups consider generational transfers of wealth and retirement needs. Likewise, the rising silver dollar will be spent on healthcare products and services.

What lessons have you learned from 2019 and how has it shaped your outlook for the year ahead?

2019 has made it evident that trying to second guess or anticipate the outcome of the trade talks is futile. The market has been disappointed on a few occasions this year.

In our experience, investing in China is always a confluence of macroeconomic and microeconomic factors.

The CSI300 Index has gained 28% year to date (to 4 December 2019) while the MSCI China Index has risen by 11% over the same period6.

This has happened despite the continued and sustained downtrend in the macro economy. It is the expectation of the government’s attitude and willingness to support the economy that determines market sentiment.

This year, macro and micro appear to have decoupled again. It also reminds us that many of China’s leading companies have done well, both operationally and in terms of stock market performance, despite a weak and challenging macro environment.

While we acknowledge that China’s growth will slow after 30 years of rapid growth, we continue to find opportunities in China’s corporate sector as China’s leading companies continue to innovate, develop new market opportunities and better products and service offerings for their customers.

Notes:

1Basic Law: the ‘one country, two systems’ principle is enshrined in the Basic Law document, which applies to Hong Kong until 2047. It protects rights such as freedom of assembly and freedom of speech and the territory’s governance structure.

2P/E multiple: price to earnings (PE) ratio is a company’s share price divided by the amount of profit it makes for each share (earnings per share, EPS) in a 12-month period. PE is expressed as a number or a multiple of EPS and is an important indication of comparative value for investors.

3 Fiscal and monetary easing: relates to polices designed to stimulate the economy; this can either be fiscal where governments spend more or tax less, or it can be monetary whereby central banks use tools such as lower interest rates or asset purchase schemes.

4Shanghai/Shenzhen Stock and Bond Connect: a collaboration between the Hong Kong, Shanghai and Shenzhen Stock Exchanges and China’s interbank bond market. The market access schemes allow international and mainland Chinese investors to trade securities in each other’s markets through the trading and clearing facilities of their home exchange.

5ADR: a certificate representing shares of a foreign stock owned and issued by a US bank. ADRs facilitate the trading of foreign-based companies’ shares in US stock markets.

6Source Bloomberg, index price returns from 31 December 2018 to 4 December 2019. Past performance is not a guide to future performance.

These are the views of the author at the time of publication and may differ from the views of other individuals/teams at Janus Henderson Investors. Any securities, funds, sectors and indices mentioned within this article do not constitute or form part of any offer or solicitation to buy or sell them.

Past performance is not a guide to future performance. The value of an investment and the income from it can fall as well as rise and you may not get back the amount originally invested.

The information in this article does not qualify as an investment recommendation.

For promotional purposes.

Leave a Reply

You must be logged in to post a comment.