Apr

2018

Disruptive technology – the return of the disrupted?

DIY Investor

11 April 2018

Despite the phrase ‘Disruptive technology’ being coined by Harvard Business School professor Clayton M Christensen in 1997, the concept has been around for centuries.

The car replacing the horse drawn carriage and the telephone making the telegram defunct are two examples from yesteryear but the advent of the internet has sped the pace up dramatically.

Just look at the music industry which has now moved onto its second digital iteration with streaming services superseding downloads.

None of this should be new news and investors are increasingly looking for ways to play the disruptive technology theme, whether buying the disruptor or selling the disrupted. This article looks at the latter and whether the disrupted can fight back.

Many pages of research have been written about the rise of electric vehicles (EVs) and their potential to eradicate the internal combustion engine. This has led to a significant derating in chemical company Johnson Matthey whose main division manufactures catalytic convertors for diesel cars and trucks.

While no doubt diesel powered cars are under structural pressure, the pace of EV penetration needs to be considered.

‘investors are increasingly looking for ways to play the disruptive technology theme, whether buying the disruptor or selling the disrupted’

How feasible is it for the UK government to ban cars with tailpipe emissions by 2050? Can the current UK electricity infrastructure support the growth in EVs? Can enough charging points be added to support EV growth? Can battery technology evolve to make EVs suitable for longer journeys?

One of the bestselling all-electric cars in the UK, the Nissen Leaf, has a range of only 124 miles and takes 7 hours to charge. There are many unknowns but investors desire to sell the disrupted can create opportunities. Johnson Matthey now trades on an attractive valuation, significantly lower than its long term average.

While we are taking the threat of EVs seriously and support their benefit to our environment, one needs to consider it in relation to Johnson Matthey’s valuation.

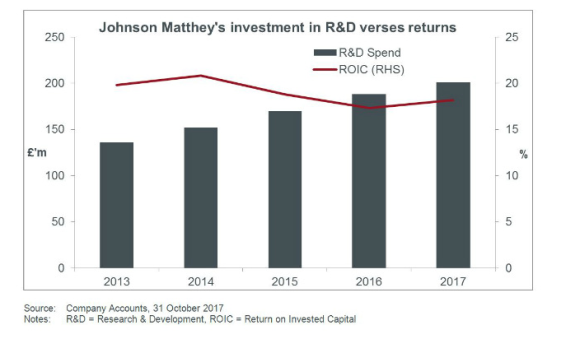

Automobile catalytic convertors only make up a quarter of the company’s revenues while there remain questions over how quickly this might trend to zero over the long term. Also the company is not standing still and has been increasing investment in research and development over the years (£850m spent in the last 5 years).

At its recent capital markets day the company talked about its next generation EV battery technology, eLNO, to challenge the NMC batteries currently being used in EVs. With claims such as better ranges, power and life cycle at a lower cost it all sounded very encouraging. No doubt there is execution risk but historically the company has delivered high teens returns on its investments.

The advent of electric cars and the fears around the impact on business models reminds me of the concerns over how e-cigarettes and vaping could have changed the face of the tobacco industry.

The tobacco companies reacted quickly, however, either buying up vaping start-ups or developing their own technologies. Although vaping continues to grow it hasn’t proved to be the disruptive force that was initially predicted.

Unfortunately it couldn’t give the same nicotine hit as traditional cigarettes, the flavours weren’t the same and the handheld devices proved unsatisfactory for some to use. This has led to the tobacco companies to continue to invest, recognising the need to find suitable alternatives to combustible cigarettes given their structural decline over health risks.

British American Tobacco is at the forefront of developing the next generation of reduced risk tobacco products called heat-not-burn (HNB).

‘investors desire to sell the disrupted can create opportunities’

The technology heats rather than burns tobacco to release a vapour with a taste similar to that of a conventional cigarette with significantly less toxicants. This gives the benefit over e-cigarettes of providing the same nicotine hit and flavour as a traditional cigarette.

It also means that the same barriers to entry of supply and distribution remain for the big tobacco companies. Soon the product will evolve with the technology used to heat the tobacco stored within a filter, meaning the delivery mechanism will match the size and feel of a tradition cigarette.

Despite this investment and growth potential, British American Tobacco’s shares have been lacklustre against a strong market in 2017. The valuation is attractive, with the company trading at a significant discount to the consumer staples sector and also offering investors a 4% dividend yield which continues to grow.

As an income investor it’s hard to own the disrupter. Those companies typically are in a growth phase and reinvest in their business rather than paying out dividends to shareholders. It’s important to remember, however, that management teams of the disrupted companies won’t necessarily stand still and the good ones will correctly balance investment to protect their businesses with dividends successfully.

Questioning the Manager: David Smith, Janus Henderson High Income Trust

Leave a Reply

You must be logged in to post a comment.